Use of Third Party Data Sources in Personal Lending

The world of personal lending is in the midst of a transformative shift. Gone are the days when a single credit score held the key to financial inclusion. Today, millions of individuals navigate a financial landscape where traditional metrics fail to capture their true creditworthiness. Underbanked, gig workers, and young adults with limited credit history – these are just a few segments often left out in the cold by lenders relying solely on outdated credit bureau data.

This reality creates a double-edged sword. Borrowers struggle to access the credit they need, while lenders grapple with the inefficiencies and limitations of a narrow view of financial health. The consequence? There is an unmet demand for credit and unrealized opportunities for both sides.

But what if there was a way to unlock the door to financial inclusion? Fortunately, there is. Enter the realm of third-party data sources, a treasure trove of alternative data points waiting to revolutionize personal lending. From income and employment verification to utility payments and online transactions, these data points offer a kaleidoscope of insights into borrowers' financial behavior, painting a far richer picture than ever before possible.

In contrast to business loans, the reasons individuals seek personal loans vary widely and include:

The spectrum of needs in a typical family mirrors the vast opportunities within the personal lending market. Applicants for these loans seek expedited processing and convenient repayment options.

The global personal loans market reached $47.79 billion in 2020 and is forecasted to surge to $719.31 billion by 2030, boasting a remarkable 31.7% CAGR from 2021 to 2030.

By embracing this data-driven approach, lenders can unlock a plethora of benefits:

-

Enhanced Credit Assessment:

No longer reliant on the limitations of credit scores, lenders can leverage alternative data to identify creditworthy borrowers who might otherwise be overlooked. This opens the door to serving new markets and expanding customer bases.

-

Improved Risk Management:

A more nuanced understanding of borrower behavior translates to more accurate risk assessment, enabling lenders to price loans more effectively and mitigate fraud risks.

-

Streamlined Lending Process:

Automated data verification from third-party sources expedites loan application review and approval, leading to faster customer on-boarding and improved operational efficiency.

-

Expanded Market Reach:

Access to alternative data empowers lenders to tap into underserved segments, fostering financial inclusion and driving market share growth.

This is not just a potential, it's a paradigm shift. Leveraging third-party data is no longer a futuristic notion, but a crucial step towards building a more inclusive and efficient lending ecosystem. In the following sections, we'll delve deeper into the types of third-party data available, explore the challenges and considerations, and offer practical strategies for lenders to navigate this exciting new world.

Stay tuned, as the next section dives into the diverse and powerful landscape of third-party data sources waiting to shape the future of personal lending.

A Spectrum of Insights: Unveiling the World of Third-Party Data

The world of alternative data in personal lending is a vibrant tapestry woven from diverse threads. Each data type offers a unique perspective, enriching lenders' understanding of borrowers beyond the confines of traditional credit scores. Let's embark on a journey through this exciting landscape, exploring the key categories that hold the potential to transform lending decisions:

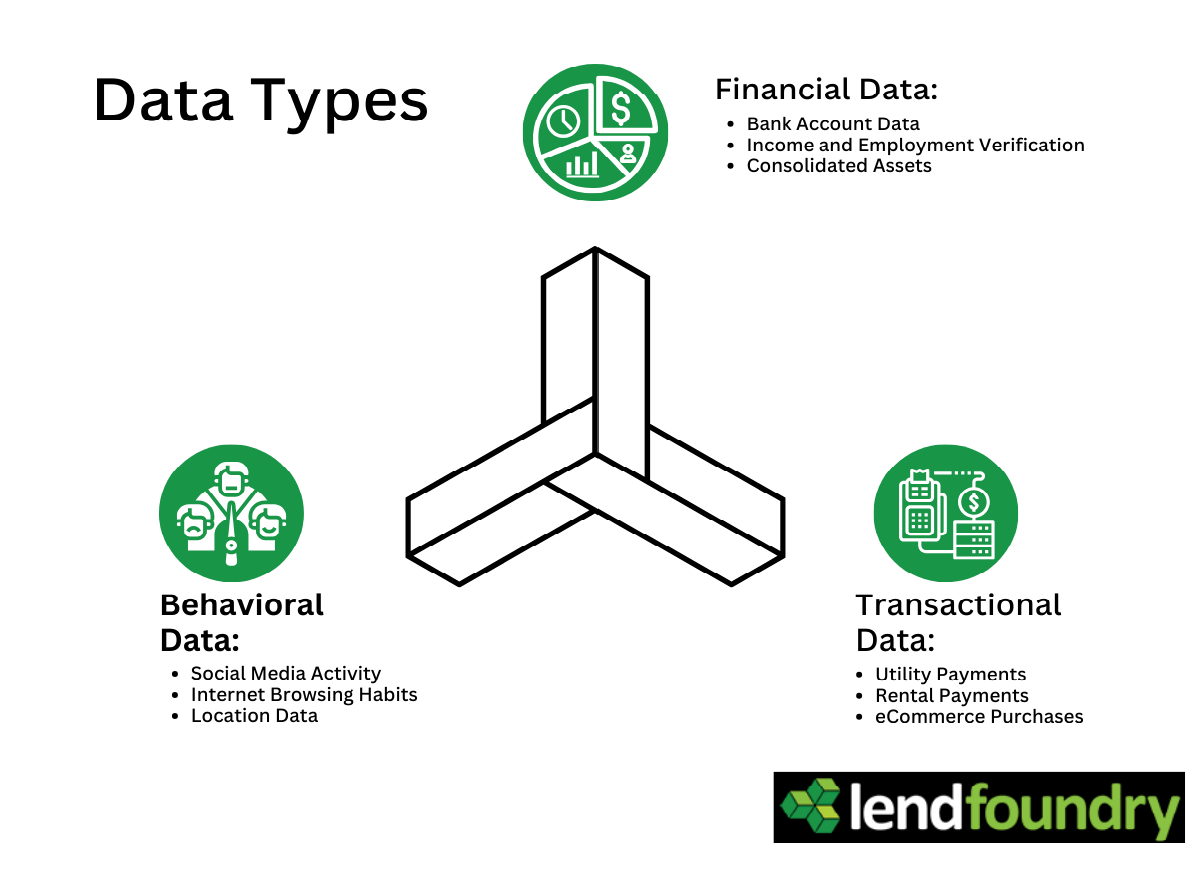

Financial Data:

- Bank Account Data: Transactions, account balances, and payment history provide a real-time glimpse into income, spending habits, and budgeting capabilities.

- Income and Employment Verification: Payroll data and tax documents offer definitive proof of income, bolstering loan applications and reducing the risk of fraud.

- Consolidated Assets: Ownership of cars, property, and investments indicates financial stability and risk tolerance, complementing the picture of creditworthiness.

Transactional Data:

- Utility Payments: Timely payments on electricity, water, and internet bills demonstrate responsible financial behavior and a commitment to meeting obligations.

- Rental Payments: Consistent rent payments, verified through third-party data providers, paint a positive picture of financial management and adherence to contractual agreements.

- eCommerce Purchases: Analyzing online shopping trends can reveal spending habits, income levels, and even potential red flags like impulse buying or excessive debt.

Behavioral Data:

- Social Media Activity: While still nascent, analyzing social media engagement and financial discussions can offer insights into financial attitudes and risk tolerance.

- Internet Browsing Habits: Browsing history may reveal financial product research, indicating loan intent and creditworthiness.

- Location Data: Location data, when used ethically and with consent, can be anonymized and aggregated to gauge economic activity and spending patterns in certain areas, informing lending decisions and market targeting.

Remember, each data type offers a single brushstroke in the larger portrait of a borrower's financial health. The magic lies in combining these diverse data points using sophisticated algorithms and data analytics to create a comprehensive and accurate assessment. This approach not only unlocks access to credit for deserving borrowers but also empowers lenders to make informed decisions, mitigate risk, and ultimately build a more sustainable and inclusive lending ecosystem.

Navigating the Rapids: Challenges and Considerations in Utilizing Third-Party Data

While the potential of third-party data in personal lending is undeniable, its integration presents a set of rapids that lenders must navigate skillfully. Here are some key challenges and considerations to keep in mind:

Data Privacy and Ethical Sourcing:

-

Ensuring Transparency and Consent:

Lenders must be transparent about the data they collect, use, and share, obtaining explicit consent from borrowers before utilizing their information.

-

Protecting Data Security:

Robust cybersecurity measures are crucial to prevent unauthorized access and ensure the data's integrity and confidentiality.

-

Avoiding Algorithmic Bias:

Algorithms used to analyze data must be rigorously tested and monitored to avoid bias against certain demographics or segments of the population.

Data Quality and Validation:

-

Accuracy and Completeness:

Ensuring the accuracy and completeness of third-party data is critical to avoid basing decisions on flawed information.

-

Data Standardization:

Different data providers may use different formats and definitions, necessitating standardization for effective analysis and integration.

-

Verifying Data Sources:

Relying on reputable and trustworthy data providers is essential to ensure the quality and reliability of the information.

Regulatory Compliance and Legal Implications:

-

Understanding Data Privacy Laws:

Each region has its own data privacy regulations, such as GDPR and CCPA, which lenders must comply with when collecting and utilizing third-party data.

-

Fair Lending Practices:

Utilizing data in a way that discriminates against certain groups is illegal and unethical. Lenders must ensure their data-driven practices adhere to fair lending principles.

-

Consumer Protection:

Transparency and fair treatment of consumers throughout the data collection and analysis process are paramount.

Addressing these challenges requires a proactive and responsible approach. Transparency, strong data governance practices, and adherence to ethical and legal frameworks are essential to unlocking the true potential of third-party data without compromising privacy, fairness, or security.

Charting the Course: Practical Strategies for Effective Implementation

Embracing third-party data in personal lending is not just about acquiring data; it's about building a sophisticated and responsible data-driven ecosystem. Here are some practical strategies to navigate this journey:

-

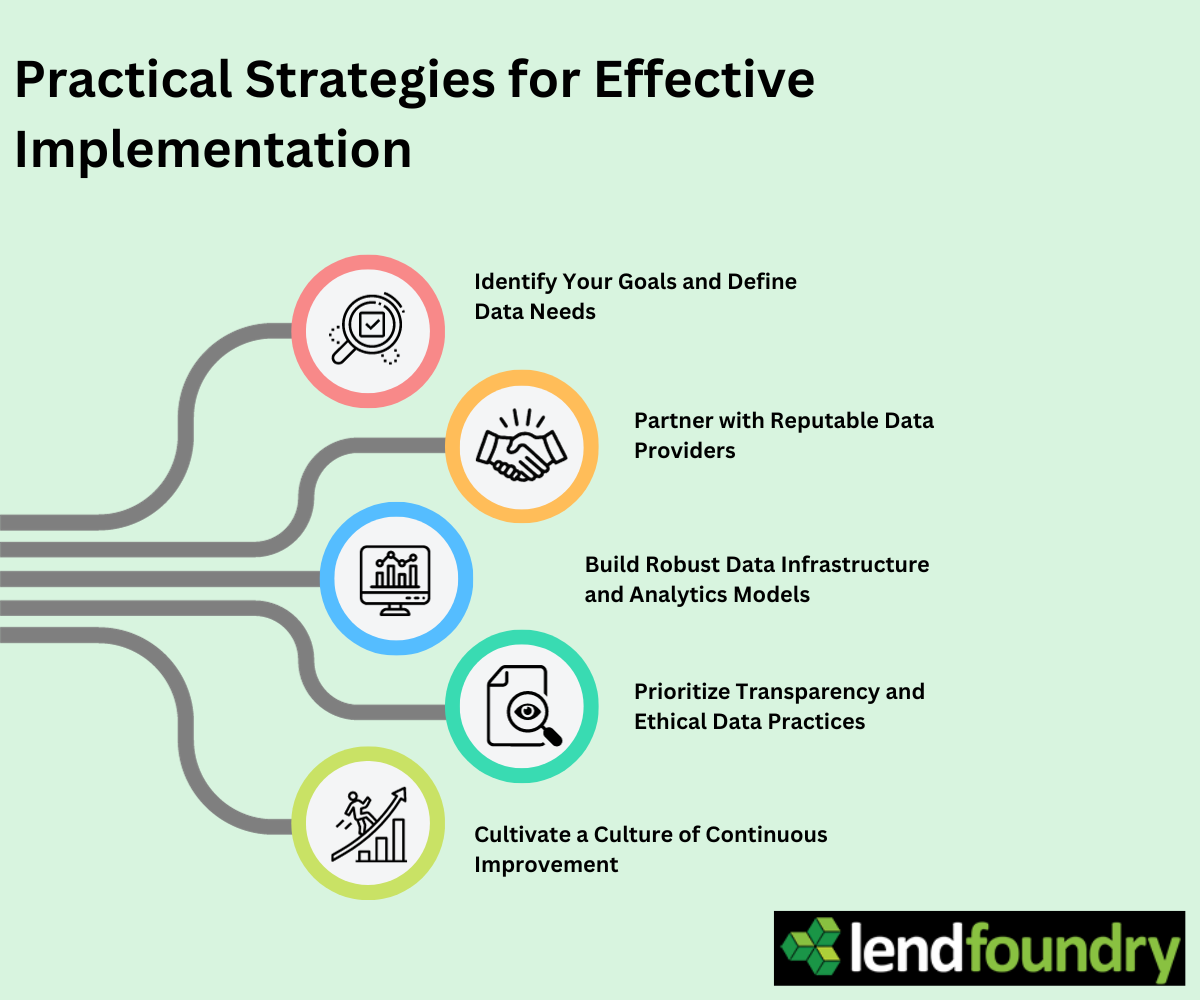

Identify Your Goals and Define Data Needs:

- Clearly define your objectives: Are you aiming to expand market reach, improve risk assessment, or streamline the lending process? Knowing your goals helps determine the specific types of data and analytics capabilities you need.

- Conduct a data needs assessment: Analyze your current loan portfolio and target customer segments to identify the data gaps that limit your decision-making.

-

Partner with Reputable Data Providers:

- Conduct thorough due diligence: Choose data providers with a strong track record of data quality, security, and compliance with relevant regulations.

- Seek expertise in specific data categories: Look for partners specializing in the data types most relevant to your goals, such as income verification or alternative credit data.

-

Build Robust Data Infrastructure and Analytics Models:

- Invest in secure data storage and analysis platforms: Ensure you have the infrastructure to process, analyze, and integrate vast amounts of data efficiently and securely.

- Develop tailored algorithms and scoring models: Leverage machine learning and data science expertise to build customized models that effectively utilize the chosen data sets for accurate credit assessment and risk prediction.

-

Prioritize Transparency and Ethical Data Practices:

- Implement clear data governance policies: Establish internal guidelines for data collection, usage, and storage, prioritizing security and user privacy.

- Ensure transparency with borrowers: Communicate openly about the data you collect and how it will be used in the lending process.

- Monitor for potential bias and discrimination: Continuously audit your algorithms and data sources to identify and mitigate any potential bias against specific demographics or groups.

-

Cultivate a Culture of Continuous Improvement:

- Embrace an iterative approach: Regularly monitor and evaluate the performance of your data-driven models.

- Stay informed about evolving regulations and data trends: Continuously adapt your data strategy and infrastructure to comply with changing regulations and leverage emerging data insights.

By taking these steps, lenders can navigate the rapids of third-party data and chart a course toward a more inclusive, efficient, and data-driven future of personal lending. Remember, responsible data utilization is not just a technological advancement; it's an ethical imperative that unlocks opportunities for both lenders and borrowers, fostering a more sustainable and inclusive financial ecosystem for all.

Unveiling the Horizon: A Data-Driven Future for Personal Lending

The landscape of personal lending is on the cusp of a data-driven revolution. By embracing the transformative power of third-party data, lenders can unlock a future brimming with possibilities:

-

Financial inclusion for all:

Underserved segments with thin credit files or alternative employment models will no longer be relegated to the financial shadows. Lenders, empowered by comprehensive data insights, can extend credit to deserving individuals who were previously overlooked, promoting economic growth and financial stability for all.

-

Smarter and faster lending decisions:

Gone are the days of slow, cumbersome loan application processes. Automated data verification and sophisticated analytics will enable lenders to make faster, more accurate credit decisions, improving customer satisfaction and operational efficiency.

-

Risk management redefined:

A deeper understanding of borrowers' financial behavior will translate into more precise risk assessment, allowing lenders to price loans competitively and mitigate potential losses, fostering a more robust and sustainable lending ecosystem.

-

Innovation and new market opportunities:

Access to alternative data will give rise to innovative lending products and services tailored to niche market segments. This, in turn, will foster competition and drive the development of new technologies and solutions, further accelerating the evolution of the lending landscape.

The journey towards this data-driven future requires conscious commitment. Transparency, ethical data practices, and responsible application of third-party data are the cornerstones upon which this future will be built. Lenders who champion these principles will unlock unparalleled growth for their businesses and contribute to a more inclusive and equitable financial system for all.

As we stand at the threshold of this new era, the question isn't if third-party data will revolutionize personal lending, but how. By embracing its potential and navigating its challenges with responsibility, the financial landscape of tomorrow promises to be one of wider access, smarter decisions, and greater opportunities for both lenders and borrowers alike.

LendFoundry isn't just about data – it's about building a responsible and inclusive lending ecosystem. We prioritize transparency, ethical data practices, and cutting-edge security measures to ensure borrower privacy and compliance with relevant regulations. LendFoundry uses cloud technology and microservices to help FinTechs create and deliver big apps quickly and easily. We have invested very significantly in Kubernetes, and other Cloud technologies to deliver a cloud-native, API-first, microservices-based digital lending technology platform for loan origination and servicing.

To learn more about our services and offerings and get the acceleration your FinTech business needs, please do contact us.